Three Things You Probably Did Not Know About Peculium and AIEVE

This is a paid-for submitted press release. CCN does not endorse, nor is responsible for any material included below and isn’t responsible for any damages or losses connected with any products or services mentioned in the press release. CCN urges readers to conduct their own research with due diligence into the company, product or service mentioned in the press release.

When Peculium released the presale ICO, many people thought that it was simply another offering that would die away. But they were wrong. The artificial intelligence being used by Peculium is the most advanced so far. It utilizes the latest technologies of machine learning to train and effect advanced cryptocurrency market analytics. Here are three things that you probably never knew about Peculium and AIEVE.

The Peculium ICO is closing on 24th January 2018

Like other ICOs, the Peculium ICO is only available during a small window of opportunity. This is the best chance to acquire the native tokens before they start trading in the exchanges. The ICO is closing on 24th January of 2018. If you buy the tokens within the remaining days, a bonus of 10% will be given.

You can access the beta version of Peculium for personal assessment

Before implementing a software-based product that is expected to have a lot of impacts, it is crucial to test everything. Peculium is using the beta version to establish whether there are issues, challenges, or problems that can be addressed before the final launch.

This video gives a detailed insight into how the Peculium platform works:

The Peculium AI can be used with any cryptocurrency

One thing that is making Peculium ICO attract a lot of interest is because of cross-platform applicability. Once you have the Peculium’s AIEVE you can easily follow any network and get prompt analytics based on market performance.

A big proportion of the cryptocurrency community has a lot of faith in Peculium ICO

As more cryptocurrencies enter the cryptocurrency market, the reality of Big Data complexity dawns. Now, Peculium’s AIEVE is here to solve the problem. This is what is endearing it to many people. Though it is true that a significant proportion wants to watch and get the assurance, there is a lot of faith and expectations from Peculium.

There Are Over 1,000 Alternatives to Bitcoin You’ve Never Heard Of

Bitcoin gets all the attention, especially since it recently rocketed towards $20,000. But many other cryptocurrencies exist, and more are being created at an accelerating rate. A quick look at coinmarketcap.com shows over 1,400 alternatives to Bitcoin (as of this writing), with a combined value climbing towards $1 trillion. So if Bitcoin is so amazing, why do these alternatives exist? What makes them different?

The easy answer is that many are simply copycats trying to piggyback on Bitcoin’s success. However, a handful have made key improvements on some of Bitcoin’s drawbacks, while others are fundamentally different, allowing them to perform different functions. The far more complicated—and fascinating—answer lies in the nitty-gritty details of blockchain, encryption, and mining.

To understand these other cryptocurrencies, Bitcoin’s shortcomings need to first be understood, as the other currencies aim to pick up where Bitcoin falls short.

The Problems With Bitcoin

Bitcoin’s block size is only 1 MB, drastically limiting the number of transactions each block can hold. With the pre-programmed time limit of 10 minutes per block being added, this gives a theoretical maximum of 7 transactions per second. Compared with Visa and PayPal’s significantly higher transactions per second, for example, Bitcoin can’t compete, and with the popularity of Bitcoin soaring, the problem is going to get worse. As of now, around 200,000 transactions are backlogged.

Bitcoin’s scalability problem is also likely to make mining more difficult and increase mining fees. Adding blocks to the blockchain requires doing an alarming amount of computation to find the solution to the SHA-256 cryptographic hash algorithm, for which the miner is rewarded with a geometrically decreasing predetermined amount of Bitcoins, currently at 12.5 per block.

However, each new block takes more computing than the last, meaning it becomes more difficult for less reward. To help offset this, miners can charge fees, and with it becoming more difficult to make a profit, the fees are only going to go up.

Because of the computing power needed to process each block, it has been estimated that each transaction requires enough electricity to power the average home for nine days. If this is true, and if Bitcoin continues to grow at the same rate, some have predicted it will reach an unsustainable level within a decade.

Furthermore, Bitcoin’s blockchain has only one purpose: to handle Bitcoin. Given the complexity of the system, it could be doing much more. Also, Bitcoin is not entirely anonymous. For any given Bitcoin address, the transactions and the balance can be seen, as they are public and stored permanently on the network. The details of the owner can be revealed during a purchase.

Altcoins

Ignoring the copycats, several Bitcoin alternatives—or altcoins—have gained popularity. Some of these are a result of changing the Bitcoin code, which is open-source, effectively creating a hard fork in the blockchain and a new cryptocurrency. Others have their own native blockchains.

Hard forks include Bitcoin Cash, Bitcoin Classic, and Bitcoin XT, all three of which increased the block size. XT changed the block size to 8 MB, allowing for up to 24 transactions per second, whereas Classic only increased it to 2 MB. While these two are now terminated due to a lack of community support, Cash is still going. Its major change was to do away with Segregated Witness, which reduces the size of a transaction by removing the signature data, allowing for more transactions per block.

Another Bitcoin derivative is Litecoin. The major changes from Bitcoin are that the creator, Charlie Lee, reduced the block generation time from 10 minutes to 2.5, and instead of using SHA-256, it uses scrypt, which is considered by some to be a more efficient hashing algorithm.

As far as native blockchains go, there are a lot of altcoins.

One of the most popular—at least by market capitalization—is Ethereum. The key element that distinguishes Ethereum from Bitcoin is that its language is Turing-complete, meaning it can be programmed for just about anything, such as smart contracts, not just its currency, Ether. For example, the United Nations has adopted it to transfer vouchers for food aid to refugees, keep track of carbon outputs, etc.

Monero has solved Bitcoin’s privacy issue. It uses ring signatures, which allow for information about the sender to hide among other pieces of data, effectively creating stealth addresses. This makes the Monero blockchain opaque, not transparent like other blockchains. However, programmers have included a “spend” key and a “view” key, which allow for optional transparency if agreed upon for specific transactions.

Dash has avoided Bitcoin’s logjam by splitting the network into two tiers. The first handles block generation done by miners, much like Bitcoin, but the second tier contains masternodes. These handle the new services of PrivateSend and InstantSend, and they add a level of privacy and speed not seen in other blockchains. These transactions are confirmed by a consensus of the masternodes, thus removing them from the computing and time-intensive project of block generation.

IOTA just did away with blocks altogether. It stands for the Internet of Things Application and depends on users to validate transactions instead of relying on miners and their souped-up computers. As a user conducts a transaction, he/she is required to validate two previous transactions, so the rate of validation will always scale with the amount of transactions.

On the other hand, Ripple, which is now one of the top cryptocurrencies by market capitalization, has taken a completely different approach. While other cryptocurrencies are designed to replace the traditional banking system, Ripple attempts to strengthen it by facilitating bank transfers. That is, bank transfers depend on systems like SWIFT, which is expensive and time-consuming, but Ripple’s blockchain can perform the same functions far more efficiently. Over 100 major banking institutions are signed up to implement it.

Bitcoin isn’t going anywhere anytime soon, but budding crypto-enthusiasts should give heed to these competitors and many others, as they may one day replace it as the dominant cryptocurrency.

Original article and pictures take singularityhub.com site

The threat of tough regulation in Asia sends crypto-currencies into a tailspin

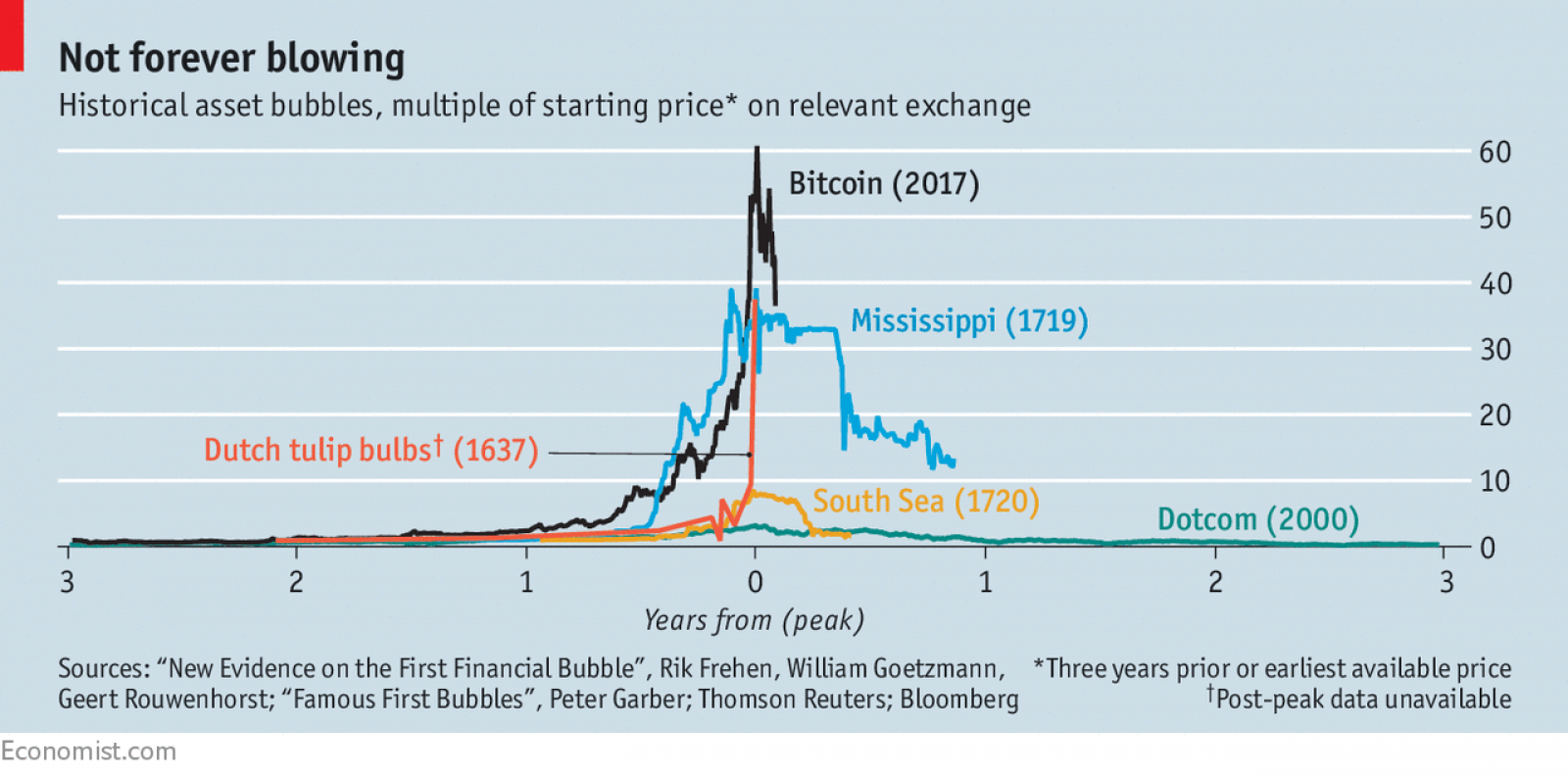

IT HAS been another week of vertiginous swings in the prices of bitcoin and other crypto-currencies. This time, the moves have mostly been downwards, with some days seeing falls of over 20%. Views on this were as divided as they were during the giddy climb: did it mark the definitive bursting of a bubble as rapidly inflated as any in history (see chart)?

Asia provides both an explanation of this week’s sell-off and a glimpse of crypto-currencies’ future. The threat of a ban in bitcoin-trading in South Korea was the proximate cause of the plunge. As to the future, the question is which Asia? At one end of the spectrum is Japan, which has embraced crypto-currencies. At the other is China, which has all but banished them. South Korea has been in the middle.

These countries have outsized roles in the crypto universe. China’s exchanges hosted more than nine-tenths of global bitcoin-trading until the government closed them last year. Japan now has the biggest share of virtual-currency markets. South Korea makes up less than 2% of global GDP but nearly a tenth of bitcoin-trading.

North Asia has been fertile ground for crypto-currencies for several reasons. Partly it is the high-tech pedigree. A prevalence of smartphones, fast internet and computer-science graduates makes people receptive to the newfangled. The rigidity of conventional finance has helped. Capital controls boost the appeal of crypto-currencies in China and South Korea, and in Japan they are a beguiling alternative to low-yielding mainstream investments. A zest for gambling has surely lured some to a market that is driven by speculation.

But the region’s regulators are going in different directions. China, alarmed at the way crypto-currencies can evade government oversight, has taken the harshest line. Last year it banned domestic exchanges; in recent days it has taken aim at websites flouting this ban. Officials have also called on local authorities to choke off the power supply to bitcoin miners, computer networks that create new coins through massively energy-intensive calculations. China’s miners, still dominant in the global industry, are shifting to other countries.

The Chinese government admires the technology that underpins virtual currencies and wants to reap the benefits. It is prodding its big financial firms to experiment with blockchain, a system of distributed ledgers popularised by bitcoin. But officials believe they can do this without having to tolerate the currencies themselves. As Pan Gongsheng, deputy governor of the central bank, quipped last year, quoting a French economist: “The only thing to do is to sit by the riverbank and wait for bitcoin’s corpse to float past.”

Japan, by contrast, has given crypto-currencies room to run. Its regulators know the dangers. One of the biggest scandals in bitcoin’s short history was the collapse of Mt. Gox, a Japan-based exchange, in 2014. And officials have not minced their words, with Haruhiko Kuroda, governor of the Bank of Japan, warning that the bitcoin rally in late 2017 was “abnormal”.

But rather than throttle virtual currencies and the innovations they might spawn, the government has let them develop, within parameters. Last March it passed the “virtual-currency act”, declaring that they are assets and can be used for payments. The financial-services authority has granted licences to 11 exchanges, to reduce the risk of fraud. Zennon Kapron, a Shanghai-based analyst of digital currencies, says that some of China’s leading crypto-coders are now moving to Japan.

South Korea was initially hands-off in its regulations. But alarm has mounted about the speculative fervour. So intense is the demand that South Koreans pay a “kimchi premium” of roughly 40% for their bitcoins (not easily arbitraged away because of capital controls). On January 11th the justice minister said crypto-currency exchanges would be banned. Their devotees responded with a petition urging leniency, which swiftly collected more than 200,000 signatures.

Faced with this backlash, the government appeared to soften its stance, saying a ban was just one idea. Other incoming measures are less potent: investors will have to pay taxes on capital gains and register trading accounts under their real names. But just as crypto-markets had recovered their poise, South Korea’s finance minister said this week that the ban was still very much on the table, calling it a “live option”. The collapse resumed.

Virtual currencies have bounced back from past sell-offs, but this has been a big one. At one point bitcoin was down about 50% from its highs in December. Believers in virtual currencies say that one of their selling points is freedom from government meddling. In Asia, the cutting edge of the crypto-world, it is governments that are making—and breaking—their fortunes.

Original article and pictures take cdn.static-economist.com site

This is a management company which maintains index fund CIV20. The CIV20 is a unique token and includes the 20 largest and is a most popular cryptocurrency. It is been updated on every Monday. The company takes care of the cost for the management of the fund. The token holder accepts dividends which are paid from the profits of the managing company GuideCTF.

The company’s capitalization depends upon the capitalization of its emitted assets. The first motto is to emit the fund token. The fund tokens can acquire the website after registration and authentication of the account. Marketing activities involved in GuideCTF such as participating in crypto and investment forums can assist to the growth and development of the company.

Original article and pictures take icoclap.com site

The real value of bitcoin and crypto currency technology - The Blockchain explained

Donations are welcome at: 1AtFaRrPFiwm2xUYN2C41edGgKPR5AXYDh

Blockchain and Bitcoin explained in five minutes: Blockchain technology will drastically change our lives.

In the coming years, Blockchain, the technology behind crypto currencies such as Bitcoin, will inevitably and radically change the role of traditional trusted parties such as banks, accountants, notaries, and governments. The animated video about Blockchain and Bitcoin that was released today on http://bitcoinproperly.org is the first to specifically address the technology behind Bitcoin: the Blockchain. Within five minutes, it is explained how the essential functions of the “trusted third party” can be automatized through the Blockchain as well as what the implications of this are.

From Bitcoin hype to Blockchain revolution: an internet of trust.

With the arrival of crypto currencies such as Bitcoin, everyone around the world can trade with each other without any involvement from traditional third parties such as banks, notaries, accountants, and governments. Trade is a fundamental pillar of our economy and society, and traditional trusted parties play a crucial role in this.

The technology behind Bitcoin making all this possible – the Blockchain – ensures that the essential functions of the “trusted third party’, are fully automatized through the internet. This way, these functions are as freely available, accessible, and programmable as the internet itself.

The animated video, available in both Dutch and English, explains how this works, also mentioning practical applications. The implications are clear: in the coming years, the role of the traditional trusted parties will inevitably and drastically change, strongly impacting our daily lives.

The creators of this animated video invite its viewers to think about and discuss the fundamental and radical innovations made possible by crypto currencies.

Rutger van Zuidam founder of Dutchchain, organizer of the Dutch Blockchain Hackathon: “The Netherlands have all the assets to become Europe’s Silicon Valley of financial technology. It is possible for the Netherlands to position itself favourably in comparison to the US and UK, who are currently still ahead. The technology behind crypto currencies like Bitcoin plays an essential role in leveraging these opportunities. We hope that the animated video about the technology behind crypto currencies will positively affect this development.”

Lykle de Vries: ”Bitcoin is not the new money for internet,but it is the new internet for money, value and ownership in all forms. Crypto currencies like Bitcoin are the next step in the emancipation of all world citizens, and can help create a new dynamic for democracy, society and economy.”

About the creators

The animated video is a non-profit initiative by designers Patrick Loonstra (www.patrickloonstra.nl) and Sebas van den Brink (sebasvandenbrink.nl) and entrepreneurs Lykle de Vries (ThesisOne.com) and Rutger van Zuidam (DutchChain.com).

Original article and pictures take s.ytimg.com site

This kind of the bitcoin transaction is providing ability to send and get money. People no need to worry about the rescheduling for the bank holidays, crossing borders and other limitations. It allows the people to control their transaction which is helping to keep your bitcoin in safe. In a modern world more than 2.2 billion people are not showing interest to access the ancient exchange transaction system. These people are interested to follow the bitcoin transaction system and it is the mobile based money transfer system. Bitcoin is not involving in the transaction fees so that you can easily save your money and effort. It is fight against the identity theft and it is having secure encryption method to secure your money. Actually digital currency exchange is useful to the trade process transactions and this process is converting the bitcoin into the fiat currency. Fortunately this kind of the services is really having low fees when compared to the PayPal and credit cards.

To know about disadvantages of the bitcoin

A coin has both face like head and tail so bitcoin has also advantages and disadvantages. The first thing limited amount of bitcoin is available in online so that people struggle to obtain this coin. The next thing people might not aware of the bitcoin concept which is the major drawback of this bitcoin. People must be educated about the bitcoin so that you can obtain the advantages available in the bitcoin. It is still in the developing stage so before you choose the bitcoin you must know about the risk involve in the bitcoin transaction system. If you are in the business industry then you must know about the bitcoin advantages and risks.

Original article and pictures take tomfoolery.info site

Blockchain, the technology underpinning bitcoin, is one of the most important innovations since the development of the Internet. It has generated a lot of interest lately and it is likely to continue in view of the broadening adoption.

The globe’s leading banks are starting to realize they need to embrace innovative technologies in order to stay competitive in today’s digitized world. Financial services providers are actively investing in various blockchain projects aimed at exploring the potential use cases of the technology.

A major software solutions provider, Sopra Banking Software, has published blockchain infographics that highlight the main benefits of the technology and analyze its potential role in the future of the banking industry.

One of the most important benefits of the cryptocurrency technology, the company stated, is that it eliminates the need to deal with intermediaries. Unlike current centralized systems, which depend on a single entity, the blockchain has no central ledger. The distributed nature of approving transactions makes it hard to compromise the system.

Voting management is one of the other areas that can be improved with the cryptocurrency technology. The use of the blockchain can retain the simplicity of electronic voting while providing an increased security. In 2015, NASDAQ CEO, Bob Greifeld, announced that the Estonian NASDAQ market will apply the blockchain to streamline the process of proxy voting.

The technology can also be used to simplify the issuance of dividends and shares, say the blockchain infographics. This year, online retailer Overstock.com secured the U.S. Security and Exchange Commission (SEC) approval for the use of the blockchain to issue company shares.

Financial organizations expect they would significantly benefit from integrating the blockchain, which offers such advantages as higher transparency, faster transactions, and lower threat of hacking attacks. Moreover, companies using the technology would be able to reduce costs of transactions settlement. As Sopra Banking Software wrote in its blockchain infographics, banks would save up to $20 billion in fees if they integrate the blockchain system.

Meantime, researchers from Greenwich Associates discovered that the majority (94%) of the interviewed financial professionals believe that the distributed ledger technology would be beneficial to institutional markets. Besides, the study found that half of the surveyed were actively reviewing the blockchain within their companies.

Share This article Original article and pictures take www.coinspeaker.com site

OPN and One Coin has become one. Dr. Ruja Ignatova, the CEO, announced it a month ago in Budapest. Both the companies have become one. Ruja was satisfied with this thing as One Coin can work alongside with a big network marketing business. The global clients and teams of that business can enjoy lots of features of One Coin. Based on the report, this crypto-currency company has grown bigger faster recently. There are many sales that have been made and thousands of members who make profits with One Coin. The opportunity is just limitless.

Even though there have been many people joining One Coin, some of us aren’t really into crypto-currency. The fact is that many people have a doubt with the digital currency. Whatever it is, the company keeps its ambition to be the next biggest crypto-currency after Bitcoin. It also utilizes the latest technology that will provide benefits for the members. This will be a long-term benefit for all of us, in fact. There’s another reason why more people are into crypto-currency. There’s no fee. The digital currency has no linkage to central banks and government. By joining One Coin, we can also get the training. This means we can learn how to make profits from it.

Register Free Today! Original article and pictures take onecoincurrencycrypto.blogspot.ie site

The Fed Created Ripple Now The Central Bank In England Wants Their Own Crypto Currency!

the Federal reserve created ripple and it has been a major success. Now the central bank of England Wants to replicate their success in creating their own crypto currency. The have already tested their crypto on blockchain last year and they have plans to have it developed within the year.

Original article and pictures take s.ytimg.com site

In 2008, the aftermath of the Subprime Mortgage Crisis created the perfect storm for the emergence of Bitcoin. This is the definitive history of the famous crypto-currency.

Original article and pictures take 2oqz471sa19h3vbwa53m33yj.wpengine.netdna-cdn.com site

There are lots of ways to make money: You can earn it, find it, counterfeit it, steal it. Or, if you’re Satoshi Nakamoto, a preternaturally talented computer coder, you can invent it. That’s what he did on the evening of January 3, 2009, when he pressed a button on his keyboard and created a new currency called bitcoin. It was all bit and no coin. There was no paper, copper, or silver—just thirty-one thousand lines of code and an announcement on the Internet.

Nakamoto, who claimed to be a thirty-six-year-old Japanese man, said he had spent more than a year writing the software, driven in part by anger over the recent financial crisis. He wanted to create a currency that was impervious to unpredictable monetary policies as well as to the predations of bankers and politicians. Nakamoto’s invention was controlled entirely by software, which would release a total of twenty-one million bitcoins, almost all of them over the next twenty years. Every ten minutes or so, coins would be distributed through a process that resembled a lottery. Miners—people seeking the coins—would play the lottery again and again; the fastest computer would win the most money.

Interest in Nakamoto’s invention built steadily. More and more people dedicated their computers to the lottery, and forty-four exchanges popped up, allowing anyone with bitcoins to trade them for official currencies like dollars or euros. Creative computer engineers could mine for bitcoins; anyone could buy them. At first, a single bitcoin was valued at less than a penny. But merchants gradually began to accept bitcoins, and at the end of 2010 their value began to appreciate rapidly. By June of 2011, a bitcoin was worth more than twenty-nine dollars. Market gyrations followed, and by September the exchange rate had fallen to five dollars. Still, with more than seven million bitcoins in circulation, Nakamoto had created thirty-five million dollars of value.

And yet Nakamoto himself was a cipher. Before the début of bitcoin, there was no record of any coder with that name. He used an e-mail address and a Web site that were untraceable. In 2009 and 2010, he wrote hundreds of posts in flawless English, and though he invited other software developers to help him improve the code, and corresponded with them, he never revealed a personal detail. Then, in April, 2011, he sent a note to a developer saying that he had “moved on to other things.” He has not been heard from since.

When Nakamoto disappeared, hundreds of people posted theories about his identity and whereabouts. Some wanted to know if he could be trusted. Might he have created the currency in order to hoard coins and cash out? “We can effectively think of ‘Satoshi Nakamoto’ as being on top of a Ponzi scheme,” George Ou, a blogger and technology commentator, wrote.

It appeared, though, that Nakamoto was motivated by politics, not crime. He had introduced the currency just a few months after the collapse of the global banking sector, and published a five-hundred-word essay about traditional fiat, or government-backed, currencies. “The root problem with conventional currency is all the trust that’s required to make it work,” he wrote. “The central bank must be trusted not to debase the currency, but the history of fiat currencies is full of breaches of that trust. Banks must be trusted to hold our money and transfer it electronically, but they lend it out in waves of credit bubbles with barely a fraction in reserve.”

Banks, however, do much more than lend money to overzealous homebuyers. They also, for example, monitor payments so that no one can spend the same dollar twice. Cash is immune to this problem: you can’t give two people the same bill. But with digital currency there is the danger that someone can spend the same money any number of times.

Nakamoto solved this problem using innovative cryptography. The bitcoin software encrypts each transaction—the sender and the receiver are identified only by a string of numbers—but a public record of every coin’s movement is published across the entire network. Buyers and sellers remain anonymous, but everyone can see that a coin has moved from A to B, and Nakamoto’s code can prevent A from spending the coin a second time.

Nakamoto’s software would allow people to send money directly to each other, without an intermediary, and no outside party could create more bitcoins. Central banks and governments played no role. If Nakamoto ran the world, he would have just fired Ben Bernanke, closed the European Central Bank, and shut down Western Union. “Everything is based on crypto proof instead of trust,” Nakamoto wrote in his 2009 essay.

Bitcoin, however, was doomed if the code was unreliable. Earlier this year, Dan Kaminsky, a leading Internet-security researcher, investigated the currency and was sure he would find major weaknesses. Kaminsky is famous among hackers for discovering, in 2008, a fundamental flaw in the Internet which would have allowed a skilled coder to take over any Web site or even to shut down the Internet. Kaminsky alerted the Department of Homeland Security and executives at Microsoft and Cisco to the problem and worked with them to patch it. He is one of the most adept practitioners of “penetration testing,” the art of compromising the security of computer systems at the behest of owners who want to know their vulnerabilities. Bitcoin, he felt, was an easy target.

“When I first looked at the code, I was sure I was going to be able to break it,” Kaminsky said, noting that the programming style was dense and inscrutable. “The way the whole thing was formatted was insane. Only the most paranoid, painstaking coder in the world could avoid making mistakes.”

Kaminsky lives in Seattle, but, while visiting family in San Francisco in July, he retreated to the basement of his mother’s house to work on his bitcoin attacks. In a windowless room jammed with computers, Kaminsky paced around talking to himself, trying to build a mental picture of the bitcoin network. He quickly identified nine ways to compromise the system and scoured Nakamoto’s code for an insertion point for his first attack. But when he found the right spot, there was a message waiting for him. “Attack Removed,” it said. The same thing happened over and over, infuriating Kaminsky. “I came up with beautiful bugs,” he said. “But every time I went after the code there was a line that addressed the problem.”

He was like a burglar who was certain that he could break into a bank by digging a tunnel, drilling through a wall, or climbing down a vent, and on each attempt he discovered a freshly poured cement barrier with a sign telling him to go home. “I’ve never seen anything like it,” Kaminsky said, still in awe.

Kaminsky ticked off the skills Nakamoto would need to pull it off. “He’s a world-class programmer, with a deep understanding of the C++ programming language,” he said. “He understands economics, cryptography, and peer-to-peer networking.”

“Either there’s a team of people who worked on this,” Kaminsky said, “or this guy is a genius.”

Kaminsky wasn’t alone in this assessment. Soon after creating the currency, Nakamoto posted a nine-page technical paper describing how bitcoin would function. That document included three references to the work of Stuart Haber, a researcher at H.P. Labs, in Princeton. Haber is a director of the International Association for Cryptologic Research and knew all about bitcoin. “Whoever did this had a deep understanding of cryptography,” Haber said when I called. “They’ve read the academic papers, they have a keen intelligence, and they’re combining the concepts in a genuinely new way.”

Haber noted that the community of cryptographers is very small: about three hundred people a year attend the most important conference, the annual gathering in Santa Barbara. In all likelihood, Nakamoto belonged to this insular world. If I wanted to find him, the Crypto 2011 conference would be the place to start.

“Here we go, team!” a cheerleader shouted before two burly guys heaved her into the air.

It was a foggy Monday morning in mid-August, and dozens of college cheerleaders had gathered on the athletic fields of the University of California at Santa Barbara for a three-day training camp. Their hollering could be heard on the steps of a nearby lecture hall, where a group of bleary-eyed cryptographers, dressed in shorts and rumpled T-shirts, muttered about symmetric-key ciphers over steaming cups of coffee.

This was Crypto 2011, and the list of attendees included representatives from the National Security Agency, the U.S. military, and an assortment of foreign governments. Cryptographers are little known outside this hermetic community, but our digital safety depends on them. They write the algorithms that conceal bank files, military plans, and your e-mail.

I approached Phillip Rogaway, the conference’s program chair. He is a friendly, diminutive man who is a professor of cryptography at the University of California at Davis and who has also taught at Chiang Mai University, in Thailand. He bowed when he shook my hand, and I explained that I was trying to learn more about what it would take to create bitcoin. “The people who know how to do that are here,” Rogaway said. “It’s likely I either know the person or know their work.” He offered to introduce me to some of the attendees.

Nakamoto had good reason to hide: people who experiment with currency tend to end up in trouble. In 1998, a Hawaiian resident named Bernard von NotHaus began fabricating silver and gold coins that he dubbed Liberty Dollars. Nine years later, the U.S. government charged NotHaus with “conspiracy against the United States.” He was found guilty and is awaiting sentencing. “It is a violation of federal law for individuals . . . to create private coin or currency systems to compete with the official coinage and currency of the United States,” the F.B.I. announced at the end of the trial.

Online currencies aren’t exempt. In 2007, the federal government filed charges against e-Gold, a company that sold a digital currency redeemable for gold. The government argued that the project enabled money laundering and child pornography, since users did not have to provide thorough identification. The company’s owners were found guilty of operating an unlicensed money-transmitting business and the C.E.O. was sentenced to months of house arrest. The company was effectively shut down.

Nakamoto seemed to be doing the same things as these other currency developers who ran afoul of authorities. He was competing with the dollar and he insured the anonymity of users, which made bitcoin attractive for criminals. This winter, a Web site was launched called Silk Road, which allowed users to buy and sell heroin, LSD, and marijuana as long as they paid in bitcoin.

Still, Lewis Solomon, a professor emeritus at George Washington University Law School, who has written about alternative currencies, argues that creating bitcoin might be legal. “Bitcoin is in a gray area, in part because we don’t know whether it should be treated as a currency, a commodity like gold, or possibly even a security,” he says.

Gray areas, however, are dangerous, which may be why Nakamoto constructed bitcoin in secret. It may also explain why he built the code with the same peer-to-peer technology that facilitates the exchange of pirated movies and music: users connect with each other instead of with a central server. There is no company in control, no office to raid, and nobody to arrest.

Today, bitcoins can be used online to purchase beef jerky and socks made from alpaca wool. Some computer retailers accept them, and you can use them to buy falafel from a restaurant in Hell’s Kitchen. In late August, I learned that bitcoins could also get me a room at a Howard Johnson hotel in Fullerton, California, ten minutes from Disneyland. I booked a reservation for my four-year-old daughter and me and received an e-mail from the hotel requesting a payment of 10.305 bitcoins.

By this time, it would have been pointless for me to play the bitcoin lottery, which is set up so that the difficulty of winning increases the more people play it. When bitcoin launched, my laptop would have had a reasonable chance of winning from time to time. Now, however, the computing power dedicated to playing the bitcoin lottery exceeds that of the world’s most powerful supercomputer. So I set up an account with Mt. Gox, the leading bitcoin exchange, and transferred a hundred and twenty dollars. A few days later, I bought 10.305 bitcoins with the press of a button and just as easily sent them to the Howard Johnson.

It was a simple transaction that masked a complex calculus. In 1971, Richard Nixon announced that U.S. dollars could no longer be redeemed for gold. Ever since, the value of the dollar has been based on our faith in it. We trust that dollars will be valuable tomorrow, so we accept payment in dollars today. Bitcoin is similar: you have to trust that the system won’t get hacked, and that Nakamoto won’t suddenly emerge to somehow plunder it all. Once you believe in it, the actual cost of a bitcoin—five dollars or thirty?—depends on factors such as how many merchants are using it, how many might use it in the future, and whether or not governments ban it.

My daughter and I arrived at the Howard Johnson on a hot Friday afternoon and were met in the lobby by Jefferson Kim, the hotel’s cherubic twenty-eight-year-old general manager. “You’re the first person who’s ever paid in bitcoin,” he said, shaking my hand enthusiastically.

Kim explained that he had started mining bitcoins two months earlier. He liked that the currency was governed by a set of logical rules, rather than the mysterious machinations of the Federal Reserve. A dollar today, he pointed out, buys you what a nickel bought a century ago, largely because so much money has been printed. And, he asked, why trust a currency backed by a government that is fourteen trillion dollars in debt?

Kim had also figured that bitcoin mining would be a way to make up the twelve hundred dollars he’d spent on a high-performance gaming computer. So far, he’d made only four hundred dollars, but it was fun to be a pioneer. He wanted bitcoin to succeed, and in order for that to happen businesses needed to start accepting it.

The truth is that most people don’t spend the bitcoins they buy; they hoard them, hoping that they will appreciate. Businesses are afraid to accept them, because they’re new and weird—and because the value can fluctuate wildly. (Kim immediately exchanged the bitcoins I sent him for dollars to avoid just that risk.) Still, the currency is young and has several attributes that appeal to merchants. Robert Schwarz, the owner of a computer-repair business in Klamath Falls, Oregon, began selling computers for bitcoin to sidestep steep credit-card fees, which he estimates cost him three per cent on every transaction. “One bank called me saying they had the lowest fees,” Schwarz said. “I said, ‘No, you don’t. Bitcoin does.’ ” Because bitcoin transfers can’t be reversed, merchants also don’t have to deal with credit-card charge-backs from dissatisfied customers. Like cash, it’s gone once you part with it.

At the Howard Johnson, Kim led us to the check-in counter. The lobby featured imitation-crystal chandeliers, ornately framed oil paintings of Venice, and, inexplicably, a pair of faux elephant tusks painted gold. Kim explained that he hadn’t told his mother, who owned the place, that her hotel was accepting bitcoins: “It would be too hard to explain what a bitcoin is.” He said he had activated the tracking program on his mother’s Droid, and she was currently about six miles away. Today, at least, there was no danger of her finding out about her hotel’s financial innovation. The receptionist handed me a room card, and Kim shook my hand. “So just enjoy your stay,” he said.

Nakamoto’s extensive online postings have some distinctive characteristics. First of all, there is the flawless English. Over the course of two years, he dashed off about eighty thousand words—the approximate length of a novel—and made only a few typos. He covered topics ranging from the theories of the Austrian economist Ludwig von Mises to the history of commodity markets. Perhaps most interestingly, when he created the first fifty bitcoins, now known as the “genesis block,” he permanently embedded a brief line of text into the data: “The Times 03/Jan/2009 Chancellor on brink of second bailout for banks.”

This is a reference to a Times of London article that indicated that the British government had failed to stimulate the economy. Nakamoto appeared to be saying that it was time to try something new. The text, hidden amid a jumble of code, was a sort of digital battle cry. It also indicated that Nakamoto read a British newspaper. He used British spelling (“favour,” “colour,” “grey,” “modernised”) and at one point described something as being “bloody hard.” An apartment was a “flat,” math was “maths,” and his comments tended to appear after normal business hours ended in the United Kingdom. In an initial post announcing bitcoin, he employed American-style spelling. But after that a British style appeared to flow naturally.

I had this in mind when I started to attend the lectures at the Crypto 2011 conference, including ones with titles such as “Leftover Hash Lemma, Revisited” and “Time-Lock Puzzles in the Random Oracle Model.” In the back of a darkened auditorium, I stared at the attendee list. A Frenchman onstage was talking about testing the security of encryption systems. The most effective method, he said, is to attack the system and see if it fails. I ran my finger past dozens of names and addresses, circling residents of the United Kingdom and Ireland. There were nine.

I soon discovered that six were from the University of Bristol, and they were all together at one of the conference’s cocktail parties. They were happy to chat but entirely dismissive of bitcoin, and none had worked with peer-to-peer technology. “It’s not at all interesting to us,” one of them said. The two other cryptographers from Britain had no history with large software projects. Then I started looking into a man named Michael Clear.

Clear was a young graduate student in cryptography at Trinity College in Dublin. Many of the other research students at Trinity posted profile pictures and phone numbers, but Clear’s page just had an e-mail address. A Web search turned up three interesting details. In 2008, Clear was named the top computer-science undergraduate at Trinity. The next year, he was hired by Allied Irish Banks to improve its currency-trading software, and he co-authored an academic paper on peer-to-peer technology. The paper employed British spelling. Clear was well versed in economics, cryptography, and peer-to-peer networks.

I e-mailed him, and we agreed to meet the next morning on the steps outside the lecture hall. Shortly after the appointed time, a long-haired, square-jawed young man in a beige sweater walked up to me, looking like an early-Zeppelin Robert Plant. With a pronounced brogue, he introduced himself. “I like to keep a low profile,” he said. “I’m curious to know how you found me.”

I told him I had read about his work for Allied Irish, as well as his paper on peer-to-peer technology, and was interested because I was researching bitcoin. I said that his work gave him a unique insight into the subject. He was wearing rectangular Armani glasses and squinted so much I couldn’t see his eyes.

“My area of focus right now is fully homomorphic encryption,” he said. “I haven’t been following bitcoin lately.”

He responded calmly to my questions. He was twenty-three years old and studied theoretical cryptography by himself in Dublin—there weren’t any other cryptographers at Trinity. But he had been programming computers since he was ten and he could code in a variety of languages, including C++, the language of bitcoin. Given that he was working in the banking industry during tumultuous times, I asked how he felt about the ongoing economic crisis. “It could have been averted,” he said flatly.

He didn’t want to say whether or not the new currency could prevent future banking crises. “It needs to prove itself,” he said. “But it’s an intriguing idea.”

I told him I had been looking for Nakamoto and thought that he might be here at the Crypto 2011 conference. He said nothing. Finally, I asked, “Are you Satoshi?”

He laughed, but didn’t respond. There was an awkward silence.

“If you’d like, I’d be happy to review the design for you,” he offered instead. “I could let you know what I think.”

“Sure,” I said hesitantly. “Do you need me to send you a link to the code?”

“I think I can find it,” he said.

Soon after I met Clear, I travelled to Glasgow, Kentucky, to see what bitcoin mining looked like. As I drove into the town of fourteen thousand, I passed shuttered factories and a central square lined with empty storefronts. On Howdy 106.5, a local radio station, a man tried to sell his bed, his television, and his basset hound—all for a hundred and ten dollars.

I had come to visit Kevin Groce, a forty-two-year-old bitcoin miner. His uncles had a garbage-hauling business and had let him set up his operation at their facility. The dirt parking lot was jammed with garbage trucks, which reeked in the summer sun.

“I like to call it the new moonshining,” Groce said, in a smooth Kentucky drawl, as he led me into a darkened room. One wall was lined with four-foot-tall homemade computers with blinking green and red lights. The processors inside were working so hard that their temperature had risen to a hundred and seventy degrees, and heat radiated into the room. Each system was a jumble of wires and hacked-together parts, with a fan from Walmart duct-taped to the top. Groce had built them three months earlier, for four thousand dollars. Ever since, they had generated a steady flow of bitcoins, which Groce exchanged for dollars, averaging about a thousand per month so far. He figured his investment was going to pay off.

Groce was wiry, with wisps of gray in his hair, and he split his time between working on his dad’s farm, repairing laptops at a local computer store, and mining bitcoin. Groce’s father didn’t understand Kevin’s enthusiasm for the new currency and expected him to take over the farm. “If it’s not attached to a cow, my dad doesn’t think much of it,” Groce said.

Groce was engaged to be married, and planned to use some of his bitcoin earnings to pay for a wedding in Las Vegas later in the year. He had tried to explain to his fiancée how they could afford it, but she doubted the financial prudence of filling a room with bitcoin-mining rigs. “She gets to cussing every time we talk about it,” Groce confided. Still, he was proud of the powerful computing center he had constructed. The machines ran non-stop, and he could control them remotely from his iPhone. The arrangement allowed him to cut tobacco with his father and monitor his bitcoin operation at the same time.

Nakamoto knew that competition for bitcoins would eventually lead people to build these kinds of powerful computing clusters. Rather than let that effort go to waste, he designed software that uses the processing power of the lottery players to confirm and verify transactions. As people like Groce try to win bitcoins, their computers are harnessed to analyze transactions and insure that no one spends money twice. In other words, Groce’s backwoods operation functioned as a kind of bank.

Groce, however, didn’t look like a guy Wells Fargo would hire. He liked to stay up late at the garbage-hauling center and thrash through Black Sabbath tunes on his guitar. He gave all his computers pet names, like Topper and the Dazzler, and, between guitar solos, tended to them as if they were prize animals. “I grew up milking cows,” Groce said. “Now I’m just milking these things.”

A week after the Crypto 2011 conference, I received an e-mail from Clear. He said that he would send me his thoughts on bitcoin in a day. He added, “I also think I can identify Satoshi.”

The next morning, Clear sent a lengthy e-mail. “It is apparent that the person(s) behind the Satoshi name accumulated a not insignificant knowledge of applied cryptography,” he wrote, adding that the design was “elegant” and required “considerable effort and dedication, and programming proficiency.” But Clear also described some of bitcoin’s weaknesses. He pointed out that users were expected to download their own encryption software to secure their virtual wallets. Clear felt that the bitcoin software should automatically provide such security. He also worried about the system’s ability to grow and the fact that early adopters received an outsized share of bitcoins.

“As far as the identity of the author, it would be unfair to publish an identity when the person or persons has/have taken major steps to remain anonymous,” he wrote. “But you may wish to talk to a certain individual who matches the profile of the author on many levels.”

He then gave me a name.

For a few seconds, all I could hear on the other end of the line was laughter.

“I would love to say that I’m Satoshi, because bitcoin is very clever,” Vili Lehdonvirta said, finally. “But it’s not me.”

Lehdonvirta is a thirty-one-year-old Finnish researcher at the Helsinki Institute for Information Technology. Clear had discovered that Lehdonvirta used to be a video-game programmer and now studies virtual currencies. Clear suggested that he was a solid fit for Nakamoto.

Lehdonvirta, however, pointed out that he has no background in cryptography and limited C++ programming skills. “You need to be a crypto expert to build something as sophisticated as bitcoin,” Lehdonvirta said. “There aren’t many of those people, and I’m definitely not one of them.”

Still, Lehdonvirta had researched bitcoin and worried about it. “The only people who need cash in large denominations right now are criminals,” he said, pointing out that cash is hard to move around and store. Bitcoin removes those obstacles while preserving the anonymity of cash. Lehdonvirta is on the advisory board of Electronic Frontier Finland, an organization that advocates for online privacy, among other things. Nonetheless, he believes that bitcoin takes privacy too far. “Only anarchists want absolute, unbreakable financial privacy,” he said. “We need to have a back door so that law enforcement can intercede.”

But Lehdonvirta admitted that it’s hard to stop new technology, particularly when it has a compelling story. And part of what attracts people to bitcoin, he said, is the mystery of Nakamoto’s true identity. “Having a mythical background is an excellent marketing trick,” Lehdonvirta said.

A few days later, I spoke with Clear again. “Did you find Satoshi?” he asked cheerfully.

I told him that Lehdonvirta had made a convincing denial, and that every other lead I’d been working on had gone nowhere. I then took one more opportunity to question him and to explain all the reasons that I suspected his involvement. Clear responded that his work for Allied Irish Banks was brief and of “no importance.” He admitted that he was a good programmer, understood cryptography, and appreciated the bitcoin design. But, he said, economics had never been a particular interest of his. “I’m not Satoshi,” Clear said. “But even if I was I wouldn’t tell you.”

The point, Clear continued, is that Nakamoto’s identity shouldn’t matter. The system was built so that we don’t have to trust an individual, a company, or a government. Anybody can review the code, and the network isn’t controlled by any one entity. That’s what inspires confidence in the system. Bitcoin, in other words, survives because of what you can see and what you can’t. Users are hidden, but transactions are exposed. The code is visible to all, but its origins are mysterious. The currency is both real and elusive—just like its founder.

“You can’t kill it,” Clear said, with a touch of bravado. “Bitcoin would survive a nuclear attack.”

Over the summer, bitcoin actually experienced a sort of nuclear attack. Hackers targeted the burgeoning currency, and though they couldn’t break Nakamoto’s code, they were able to disrupt the exchanges and destroy Web sites that helped users store bitcoins. The number of transactions decreased and the exchange rate plummeted. Commentators predicted the end of bitcoin. In September, however, volume began to increase again, and the price stabilized, at least temporarily.

Meanwhile, in Kentucky, Kevin Groce added two new systems to his bitcoin-mining operation at the garbage depot and planned to build a dozen more. Ricky Wells, his uncle and a co-owner of the garbage business, had offered to invest thirty thousand dollars, even though he didn’t understand how bitcoin worked. “I’m just a risk-taking son of a bitch and I know this thing’s making money,” Wells said. “Plus, these things are so damn hot they’ll heat the whole building this winter.”

To Groce, bitcoin was an inevitable evolution in money. People use printed money less and less as it is, he said. Consumers need something like bitcoin to take its place. “It’s like eight-tracks going to cassettes to CDs and now MP3s,” he said.

Even though his friends and most of his relatives questioned his enthusiasm, Groce didn’t hide his confidence. He liked to wear a T-shirt he designed that had the words “Bitcoin Millionaire” emblazoned in gold on the chest. He admitted that people made fun of him for it. “My fiancée keeps saying she’d rather I was just a regular old millionaire,” he said. “But maybe I will be someday, if these rigs keep working for me.” ♦

Original article and pictures take www.newyorker.com site

The Blockchain Technology Explained - The real value of blockchains and crypto currency technology

Catenis Enterprise by Blockchain of Things uses the power of the underlying global Bitcoin Blockchain decentralized peer-to-peer network to enables transactions, secure messaging, governance, chain of custody and disintermediation of trust. Crucial elements for the success of devices on the Internet of Things (IoT) and the industrial internet. Catenis excels at making it simple to integrate with the Bitocin Blockchain

Original article and pictures take s.ytimg.com site

![The Inevitable Blockchain [Infographic]](https://www.coinspeaker.com/wp-content/uploads/2016/11/inevitable-blockchain-infographic-full.png)